Undo Altman, Yipit brain, and is Microsoft unstoppable in AI?

19 November 2023 | Issue #16 - Mentions $MSFT, $SE, $GOOG, $AAPL, $AMZN, $META

Welcome to the sixteenth edition of Tech takes from the cheap seats. This will be my public journal, where I aim to write weekly on tech and consumer news and trends that I thought were interesting.

Let’s dig in.

Altman + Backspace (thanks to Jack Atherton at JPM for the inspo)

Given the news about Sam Altman's firing and potential return that broke over the weekend, Monday's events feel like a lifetime ago. It was just this past Monday that Altman had an interview with the Financial Times, where he discussed plans to secure additional funding from Microsoft to support his vision for achieving artificial general intelligence (AGI).

In an interview with the Financial Times, Altman said his company’s partnership with Microsoft’s chief executive Satya Nadella was “working really well” and that he expected “to raise a lot more over time” from the tech giant among other investors, to keep up with the punishing costs of building more sophisticated AI models.

Microsoft earlier this year invested $10bn in OpenAI as part of a “multiyear” agreement that valued the San Francisco-based company at $29bn, according to people familiar with the talks.

Asked if Microsoft would keep investing further, Altman said: “I’d hope so.” He added: “There’s a long way to go, and a lot of compute to build out between here and AGI . . . training expenses are just huge.”

Altman said “revenue growth had been good this year”, without providing financial details, and that the company remained unprofitable due to training costs. But he said the Microsoft partnership would ensure “that we both make money on each other’s success, and everybody is happy”.

This interview is certainly viewed in a different lens after everything that’s happened in the last 48 hours. I’ll highlight interesting snippets below.

Altman, meanwhile, splits his time between two areas: research into “how to build superintelligence” and ways to build up computing power to do so. “The vision is to make AGI, figure out how to make it safe . . . and figure out the benefits.”

Pointing to the launch of GPTs, he said OpenAI was working to build more autonomous agents that can perform tasks and actions, such as executing code, making payments, sending emails or filing claims.

“We will make these agents more and more powerful . . . and the actions will get more and more complex from here,” he said. “The amount of business value that will come from being able to do that in every category, I think, is pretty good.”

Altman said there had been “a brutal crunch” all year due to supply shortages of Nvidia’s $40,000-a-piece chips. He said his company had received H100s, and was expecting more soon, adding that “next year looks already like it’s going to be better”.

However, as other players such as Google, Microsoft, AMD and Intel prepare to release rival AI chips, the dependence on Nvidia is unlikely to last much longer. “I think the magic of capitalism is doing its thing here. And a lot of people would like to be Nvidia now,” Altman said.

Altman said his team believed that language was a “great way to compress information” and therefore developing intelligence, a factor he thought that the likes of Google DeepMind had missed.

“[Other companies] have a lot of smart people. But they did not do it. They did not do it even after I thought we kind of had proved it with GPT-3,” he said.

Ultimately, Altman said “the biggest missing piece” in the race to develop AGI is what is required for such systems to make fundamental leaps of understanding.

“There was a long period of time where the right thing for [Isaac] Newton to do was to read more math textbooks, and talk to professors and practice problems . . . that’s what our current models do,” said Altman, using an example a colleague had previously used.

But he added that Newton was never going to invent calculus by simply reading about geometry or algebra. “And neither are our models,” Altman said.

“And so the question is, what is the missing idea to go generate net new . . . knowledge for humanity? I think that’s the biggest thing to go work on.”

While the OpenAI board's aims to responsibly advance AI are admirable, we ultimately live in a capitalist society driven by financial returns. Sam Altman's firing appears tied to disagreements over AI safety, development speed, and commercialization per Bloomberg reporting. As OpenAI's largest backer at $10 billion invested, Microsoft is a for-profit company accountable to shareholders. They likely took issue with the ouster of the CEO of their multi-billion dollar investment, if it was due to limiting near-term revenue generation.

This also poses challenges for attracting future investors seeking returns, especially given Sam Altman has suggested OpenAI may seek up to $100 billion more to achieve artificial general intelligence. I suspect when Sam returns to the CEO role, some restructuring will aim to address these conflicting incentives. It will be fascinating to observe how OpenAI reconciles its noble aspirations with capitalist realities.

Related: Meta Splits Up Its Responsible AI Team, Nvidia upgrades flagship chip to handle bigger AI systems, OpenAI Pauses New Signups to Manage Overwhelming Demand

Curious case of YipitData

This week, Sea Limited reported third quarter results that were mostly in-line with Wall Street expectations. Revenue beat consensus estimates by 4%, though EBITDA missed by $45 million as the company ramped up growth investments in Q2. So why did the stock sell off over 20%? Let's look at some important context first.

As I wrote previously, Sea was in profit mode earlier this year. When they began shifting strategy, the company stopped disclosing Gross Merchandise Value (GMV) for its ecommerce division - likely to discourage overemphasis on this metric as the key indicator of business health. During the pandemic boom, Sea's stock price was rewarded for pursuing growth at all costs. It expanded aggressively into many new countries, prioritizing user acquisition over sustainable economics. But in its recent pivot towards profitability, Sea exited many unprofitable markets to focus on core regions with clearer paths to attractive unit economics. They also raised payback thresholds on marketing spend, targeting higher-value customers rather than broad reach. This pruning resulted in shedding low-quality, unprofitable orders - a headwind for overall GMV growth.

GMV disclosure stopped in Q1 2023, but alternative data providers like YipitData continued estimating it. Their GMV proxy has proven generally accurate over time, with a typical variance of only 1-2%. Yipit estimated 13% GMV growth for Q3, and 30-35% growth quarter-to-date for Q4.

Now back to why the shares sold off. Upon its return to growth mode, management have stated that they will be ramping up investments in sales and marketing to capture the massive opportunity it sees in its markets and aggressively take share while its competitors are pulling back on spend in their bid to get profitable. Investors gave feedback to the company to resume GMV disclosure so that they could gain confidence that the spend would amount to market share gains. With the latest results, Sea disclosed Q3 GMV of $20.1 billion, up just 5% year-over-year - trailing estimates by 8 full percentage points. The wide miss casts doubt on the recent Q4 strength suggested by third-party data.

So why the huge divergence between Sea's reported results and Yipit's alternative datasets? I suspect it partly stems from an increased mix of livestream orders within GMV. Currently, YipitData’s methodology to estimate GMV involves scraping data from the ecommerce website to gauge units sold and average sale prices (ASP) and then data analysis to fill in any blanks. When the company was disclosing GMV, it allowed for the methodology to be refined over time to account for any errors or lack of coverage. When the disclosure stopped, there was no longer a baseline or actual number to refer back to, to determine if the methodology was still accurate.

I think part of the reason for the divergence is due to the increasing mix of live streaming orders. During its Q3 results call, management disclosed that in Southeast Asia, average daily orders from livestreaming reached more than 10% of the total order volume in October. Web scraping price data from the website misses significant discounts on goods being sold via livestreaming, which in some cases can be over 50% cheaper than listed prices. This meant that Yipit was using headline prices and potentially overestimating average sale price (ASP) on 10% of total orders, and hence growth. This theory is reinforced by another alt data firm correctly predicting Sea's Q3 GMV using email receipt tracking rather than web scraping.

Did the 8 point miss to GMV merit a 20% stock drop? I would argue no. but some pointed to the 50% year-over-year ($430 million quarter-over-quarter) marketing spend increase driving only 5% year-over-year ($2 billion quarter-over-quarter) GMV growth. Let’s revisit a chart from my previous Sea earnings write-up, now updated with Q3 numbers.

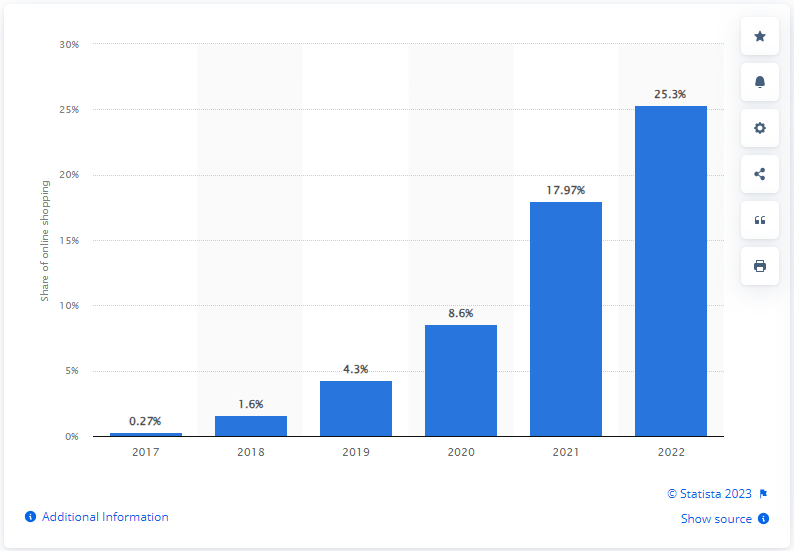

Marketing efficiency has indeed taken a hit, with every $1 of S&M spent converting to $8.4 of incremental gross GMV (that is, after accounting for churn, which I estimate to be 29% quarterly), down from $13.6 in the prior quarter. Much of this is due to the investment the company is making in livestreaming e-commerce, which management believe will become a sizable and profitable part of the platform and extends their long-term growth potential. Indeed, If we look to China as a comparison, livestreaming e-commerce has grown rapidly, and now makes up over 25% of total GMV.

Proportion of livestreaming e-commerce's GMV in online shopping in China from 2017 to 2022

Livestreaming didn't just become an opportunity this year - Shopee began building infrastructure to support it back in 2018, launching the feature in early 2019. But it failed to gain traction until TikTok arrived with its social shopping capabilities. TikTok solved the missing piece - a broad content creator network. While Shopee and Lazada had the ecommerce platform and users, they lacked creators to showcase products. Once TikTok demonstrated the format's potential, Shopee moved to invest in scaling up livestreaming to avoid losing mindshare.

Similar to launching its broader ecommerce operations, Shopee must frontload marketing spend to grow the livestream channel. Beyond typical discounts and promotions, it requires investing in content costs. Livestreaming necessitates compensating creators to host shows and make videos, via commissions and fees. Shopee is also spending on ads to promote this new format. As higher-funnel investments, these don't immediately translate to GMV.

Should investors be concerned Shopee is reverting to its old "growth at all costs" ways? I don't think so. As the efficiency chart shows, marketing spend is still above levels when aggressively expanding in to new markets. For context, when Shopee entered a new market like Poland, it offered free delivery, 0% commission for merchants, spent on marketing via TV ads, social media, the whole works. Unlike those efforts starting from zero, Shopee now has an established merchant and user base. So new livestreaming GMV should carry higher revenue.

To help alleviate concerns from investors, Chris Feng, group president of Shopee, joined the earnings call for the first time to answer Q&A. He laid out the company’s philosophy for marketing investments.

“I think, for the first question about the Q3 investment, there are two main areas that we're investing on, number one, to grow our market share, especially in the core categories, like fashion and health and beauty. The second area we're investing on is to capture the market opportunity to grow the content ecosystem, especially with the live stream first. As Forrest shared earlier, we always balance between the growth, profitability, and market share. We believe that this is the right time to invest in terms of looking at market share growth. We do see a great traction in our investments reflected from the market share gains, even with the better unit economics compared to our regional competitors.

On the content side, we believe this can be a profitable and also a very sizable businesses for us over time. If you look at the timing, as shared in the previous answers, we do see this is a good opportunity in terms of time – window of opportunity for us to capture the market, as they have been a lot more educated by having investments from various parties in the past year. For example, the viewers who understand the concept, the sellers who have the capability to offer the content, and also the ecosystem players, like the MCN (Multi-Channel Networks), et cetera.

In the past few months, since we started to invest more into the areas, we've seen very good growth in terms of the adoption of our live stream services, both on the demand side and on the supply side, not only from the creators, but also from the sellers. We also see – on top of that, which is also important to highlight, we see a significant improvement on the unit economics of our live streams. Of course, when we first started building the ecosystem, it takes a big cost to build up, but we quickly see the economics improve month-to-month actually much better than we thought before we started the program.

Overall, I guess, to answer your question, we are very happy with what we have achieved. Essentially, we achieved the market share gain, as we wanted, with much better economics than we thought. We also have seen a good traction in live stream. The take rate has been faster than we thought for the live stream services.

On the – to your question on the Q4 outlook, we will continue to invest into the shopping season. It's a holiday season, shopping season, as we all know. Q4, in our market, generally is the best time of the year to acquire new users, gain market share, and strengthen our content ecosystems. If we look at in the past one-and-a-half months, we have seen very good traction. For example, I think we shared today that – or yesterday essentially, for our Double 11, we have achieved more than $1 billion GMV, which is a very good result from – better than anticipated, especially it's over the weekend as well.”

….

In terms of the live stream percentage (penetration of e-commerce), the percentage I think mentioned in the earlier comment was for the region. If we look forward, I think the percentage of the penetration might be country by country. So, if you put everything together, it might not be fair. Let's take a look – if you take the biggest market, like Indonesia, the way we look at things, as we look at the content, e-commerce as a whole, contents including live streaming, including videos, actually which is another part of the – important part of the content. If you look at everything together, in Indonesia as a market, we do believe, let's say, somewhere range around 20% to 30% is a reasonable range we look at. Probably, it's still a little bit kind of lower than where you see from China, but has a reasonable size.

So, we know the livestream opportunity can be substantial, and based on prior management commentary, it appears incremental to core ecommerce along both user and GMV dimensions. Management has also indicated unit economics are improving and marketing efficiency may have bottomed. Additionally, Q4 growth seems to have accelerated significantly year-over-year, based on call comments about Q3 to Q4 sequential growth. This translates to around mid-20s% GMV growth compared to Q4 last year.

In terms of the growth over the quarter, I think, we don't have a detailed month-to-month breakdown on those yet. But in general, if you look at the year-to-year growth, we do see a better year-to-year growth over the months. For Q4, we do see the trend continues. So far, as we are right now, we see broadly similar trend on – in terms of the growth levels floating from Q3 to Q4, and there are impact on forex. Generally, I think the number we shared is in the US terms. But if you take the constant currencies, we actually grow better. In quite many markets actually there is depreciating against the US dollar. So, operationally, if we take the constant currency, we grow better than the US dollar basis.

Livestreaming doesn’t change the overall economics of the business either. Chris Feng has stated that terminal margins for Shopee will still be in the (previously stated) 2-3% EBITDA range as a percentage of GMV.

Regarding the question on the long-term profitability, there's no particular change to our previous views. I think you mentioned live stream, if we look at live stream in particular, we believe this is a profitable business over time. I think we have already seen the unit economic improving a lot in the past few months in my – I've shared in the last remark. It's true that there is a higher content creation cost associated with these businesses. However, there's another aspect to this as well. Number one, the product categories that does well on live stream tend to be high margin categories. Typically, the room of the margin still a bit better for those categories. So, we have better monetization capabilities from the platform. That's one.

Second one is, typically, live stream is also a good tool for sellers to drive more engagement with their buyers or potential buyers, increasing conversions, and also drive more sales during – for particular product or testing a new product or for the leftover stock, et cetera. So, generally, it's a good channel for the seller to invest themselves to market their businesses. I think, all in all, if you put everything together, we do believe that e-commerce EBITDA potential that we shared before will stay.

Taking all of this into account, Sea Limited's stock looks incredibly attractive at current levels. With a share price around $37.60, Sea has an enterprise value of $17.4 billion. Sea's Digital Entertainment segment, which includes gaming, is generating $940 million in annualized EBITDA. Gaming bookings appear to have bottomed out (growing 1% qoq), providing a stable base.

Meanwhile, Sea's Digital Financial Services business (fintech) produces $663 million in run-rate EBITDA and is still growing top-line revenue at 37% year-over-year. If we apply an 8x multiple to the stable gaming EBITDA, that implies a $7.5 billion valuation for that segment. That would leave around $10 billion of enterprise value for Sea's ecommerce and fintech businesses.

In Q4, Sea's ecommerce division Shopee is on pace for $90 billion in gross merchandise volume (GMV). We're currently in an investment period, so EBITDA is depressed. But we've seen this business reach profitability previously, so we know it can be profitable again when management pursues it. Even applying a conservative normalized margin results in a single digit EBITDA multiple for ecommerce + fintech at the current valuation.

As I've noted before, Sea deserves some discount compared to Latin American ecommerce leader MercadoLibre, which trades at 23x EBITDA. But even at half of MercadoLibre's multiple, Sea has significant upside from today's levels given the long-term growth outlook.

Disclosure: I hold shares in Sea Limited.

Related: TikTok in talks with Indonesian e-commerce firms about partnerships -minister

Google is not a monopoly continued…

We’ve always known that Apple’s bargaining power relative to other phone manufacturers was higher due its more affluent consumer base. New details emerging from the Department of Justice trial are helping quantify just how substantial Apple’s advantage is.

Google pays Apple Inc. 36% of the revenue it earns from search advertising made through the Safari browser, the main economics expert for the Alphabet Inc. unit said Monday.

Kevin Murphy, a University of Chicago professor, disclosed the number during his testimony in Google’s defense at the Justice Department’s antitrust trial in Washington.

John Schmidtlein, Google’s main litigator, visibly cringed when Murphy said the number, which was supposed to remain confidential.

I recommend reading this piece from Ben Thompson if you haven’t already. But to put some of these numbers into perspective, Alphabet currently earns about 75% gross margins from advertising on its Google properties. However, this deal suggests its gross margins from iOS are only 64% - otherwise dilutive for the ad segment. This reflects the relative power that Apple holds over Google. It does also suggest that there is competition in the search engine market as Kevin Murphy’s testimony highlights.

“The payments that Google makes reflect that competition”

He makes a good point. Why would Google agree to the deal with Apple, which dilutes their overall ad margins, if there was no competition in search? If anything, this highlights Apple’s power. I'm really looking forward to what comes out if the Department of Justice ever sues Apple for antitrust violations.

Amazon ad deals continued…

Last week, I wrote about how Meta got another win after Amazon announced its partnership with the company.

Additionally, the integration provides more first-party data for Meta. By enabling direct on-platform purchases, Meta can now link specific ad exposures directly to resulting sales. This gives Meta valuable conversion data to optimize ad targeting and measure ROI, complementing the targeting capabilities of its AI systems.

The Information came out with an article during the week that runs counter to this.

But for Meta, the deal’s benefits are limited. The arrangement does not give Meta access to data about what users end up buying, considered the holy grail for platforms because it allows them to understand whether an ad prompted someone to go through with a purchase. A notice shown to users when they first link their Amazon account with their Meta account states that the retailer will not share with Meta “specific shopping actions like purchases, product views or searches in Amazon’s stores.”

Meta has already felt the effects of being shut out of this type of data: When Apple cracked down on ad targeting by platforms like Meta and Snap with software updates in 2021, Meta had to rely on data it gathers on its own apps to target ads. Meta estimated the hit from the Apple changes amounted to a $10 billion loss in revenue.

Still, Meta will receive some data through the Amazon ads, which it can use to improve ad targeting. According to the prompt shown to users, Amazon will share with Meta whether a user is a Prime member, so Meta can show them “real-time pricing [and] delivery estimates,” as well as an estimate of the value of the Amazon product ads, “so Meta can provide you with more relevant ads.”

The article also noted that Amazon is Meta's biggest advertiser, spending hundreds of millions of dollars per year on ads. However, this may not be accurate, considering that some brokers estimate Temu has spent over $1 billion on Meta ads year-to-date. Still, the article highlighted concessions Meta has had to make for Amazon given their status as a major advertiser, which hasn’t previously been disclosed.

As a big-spending advertiser on Meta, Amazon has long had an upper hand over the social media giant. It has used its status as a major advertiser to win concessions. Several years ago, when Meta was known as Facebook, it pushed advertisers to add a piece of code known as Facebook Pixel on their websites. Pixel tracked what shoppers were viewing and buying, and then sent the data back to the company so it could hone its system for targeting ads and measuring their effectiveness.

Amazon did not want to use Pixel, mostly because it didn’t want to contribute data to Meta’s general system for optimizing ad targeting and delivery for the many companies that advertised on Meta’s apps. From Amazon’s point of view, the inclusion of its data in Meta’s systems would end up benefiting rivals that also advertise on Facebook and Instagram.

In response to Amazon’s objections, Meta quietly carved out a separate system for helping Amazon effectively run ads on Meta’s apps without using Pixel, two people with direct knowledge said. Concerned about the appearance of anti-competitive behavior, Meta kept word of the arrangement under wraps, one of the people said. The arrangement has not been previously reported.

Related: Amazon Reaches Deal to Run Shopping Ads on Snap, Shein’s Revenue Surged More Than 40%, Likely Surpassing Zara, ByteDance Revenue Surges to $29 Billion in Second Quarter, Closing in on Meta

Models as a Service

While Ben Thompson has written about Microsoft and its opportunity to become a fully integrated provider for AI use cases, recent announcements suggest they’re still hedging their bets in a way as it relates to Large Language Model providers.

We are excited to announce the upcoming preview of Models as a Service (MaaS) that offers pay-as-you-go (PayGo) inference APIs and hosted fine-tuning for Llama 2 in Azure AI model catalog. We are expanding our partnership with Meta to offer Llama 2 as the first family of Large Language Models through MaaS in Azure AI Studio. MaaS makes it easy for Generative AI developers to build LLM (Large Language Models) apps by offering access to Llama 2 as an API. We are dramatically reducing the barrier for getting started with Llama 2 by offering PayGo inference APIs billed by the number of tokens used. It takes just a few seconds to create a Llama 2 PayGo inference API that you can use to explore the model in the playground or use it with your favorite LLM tools like prompt flow, Sematic Kernel or LangChain to build LLM apps. MaaS also offers the capability to fine-tune Llama 2 with your own data to help the model understand your domain or problem space better and generate more accurate predictions for your scenario, at a lower price point. The Llama 2 inference APIs in Azure have content moderation built-in to the service, offering a layered approach to safety and following responsible AI best practices.

We aim to make Azure the best platform for developing Generative AI applications by providing seamless access to cutting-edge Large Language Models (LLMs). We are announcing Models as a Service soon to enable model providers to offer their LLMs on Azure, kicking off with Meta’s Llama 2 family of models. Traditionally, VMs with high-end GPUs meant for hosting frontier LLMs are capable of generating thousands of tokens per second but can be prohibitively expensive for dev-test cycles. MaaS eliminates the need to host models in dedicated VMs, especially for developers who don’t need high throughput during the dev-test phase of their projects. With PayGo inference APIs that are billed based on input and output tokens used, MaaS makes getting started easy and pricing attractive for Generative AI projects. Additionally, Llama 2 models can be fine-tuned with your specific data through hosted fine-tuning to enhance prediction accuracy for tailored scenarios, allowing even smaller 7B and 13B Llama 2 models to deliver superior performance for your needs at a fraction of the cost of the larger Llama 2-70B model.

I highly recommend reading the Stratechery piece if you haven’t already, but BT notes the following risk to Microsoft’s integrated approach:

This isn’t an approach without risk: Microsoft is obviously pot-committed to OpenAI, and is further making a bet that OpenAI’s model will be one of the biggest winners; it’s possible we look back in a decade and open source and company-specific models are a much larger market, and a more general purpose solution like AWS ends up being the big winner. That would fit the Christensen theory of integration and modularization, which posits that integrated products win at the beginning when solutions are not good enough, but ultimately lose out to modularized products that are more customizable and cost-effective. Even then, though, Microsoft’s cost advantage during the AI buildout (because of their ability to maximize utilization because of their mix of products across consumer, enterprise, and developers) could mean they are decently positioned to simply win on scale.

With its Model as a Service offering, it seems like Microsoft can have its cake and eat it too. While Microsoft's consumer products can benefit from tight integration with OpenAI, its enterprise service is looking to become open and modular, similar to AWS' Bedrock service. Microsoft appears well-positioned to lead the AI race, as it has been able to adapt existing theories of innovator’s solutions to its advantage. No wonder the company is making significant efforts to get Sam Altman back in his leadership role at OpenAI.

Related: Microsoft Unveils AI Chip as It Seeks to Catch Up to Nvidia, Amazon, Microsoft Ignite 2023: Copilot AI expansions, custom chips and all the other announcements

That’s all for this week. If you’ve made it this far, thanks for reading. If you’ve enjoyed this newsletter, consider subscribing or sharing with a friend

I welcome any thoughts or feedback, feel free to shoot me an email at portseacapital@gmail.com. None of this is investment advice, do your own due diligence.

Tickers: MSFT 0.00%↑ , SE 0.00%↑ , GOOG 0.00%↑ , AAPL 0.00%↑ , AMZN 0.00%↑ , META 0.00%↑

Excellent!